A few weeks ago I read a fantastic blog post by Venkat Rao titled “A Brief History of the Corporation: 1600 to 2100” (hat tip to Paul Kedrosky for the lead).

Apart from just being a great read, the macro thesis of the post — that the corporation is no longer the primary locus of commercial innovation — feels powerfully true in my little corner of the global economy: the one occupied by seed-stage software entrepreneurs, angel investors and venture capitalists.

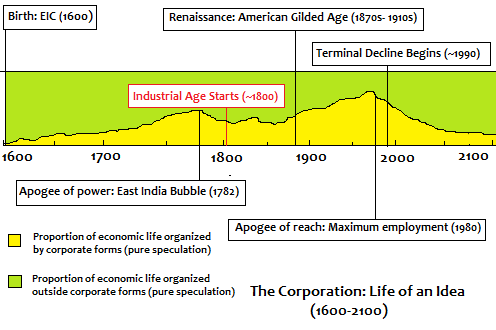

You have to read Rao’s post in its entirety to fully grok his framework (and particularly the idea of post-corporate “Cosean Growth”) but the crux of the argument is that the multi-national corporation has been displaced as the primary engine of economic development. Instead, innovation and job creation are increasingly being driven by the collective efforts of:

“the hundreds of entrepreneurs, startup-studios and incubators, 4-hour-work-weekers and lifestyle designers around the world, experimenting with novel business structures and the attention mining technologies of social media…”

Rao’s thesis helps to explain the glaring mismatch between two macroeconomic trends:

- While much of the first world is in an employment crisis, with long-term, structural unemployment figures in double-digits…

- …the market for early-stage startups — with widespread hand-wringing about early stage valuation bubble and the war for talent — is as hot as I’ve seen it since the late 1990’s

As the chart below illustrates (also from Rao’s post, but based on data from Gareth Morgan’s Images of Organization and Dan Pink’s Free Agent Nation), after peaking around 1980, the share of the U.S. workforce represented by corporate payrolls has been in free-fall for the past 30 years:

While some of this change is attributable to cyclical changes in employment, the secular trend reflects a fundmental change in the composition of the workforce. Among many the most-skilled modern knowledge workers — e.g, software developers, online marketing experts, data scientists and user experience designers — full-time employment in someone else’s company is no longer a widely-held career aspiration. In fact, the opposite is more often true: “working for the man” is just something you do to gain experience and load up your bank account before setting off on your “real” career, either as a co-founder and owner of your own enterprise, or a free-agent service provider, picking up contracts with loose teams of collaborators, solving the client’s problem and moving on to the next interesting gig.

It’s a poorly-kept secret of the tech M&A business that successful startup founders rarely stick around post-acquisition to become key players in the acquiring company. At best, they’ll fulfill the obligations of their earnout — usually a two-year stint — before cycling out to start their next company. Much like a developer taking advantage of available platforms like Twitter, Facebook, iOS or Android to accelerate growth and shorten development cycles, acquired entrepreneurs are treating their acquirers like strategic business platforms, leveraging their huge capital bases, global distribution channels and organizational support capabilities to rapidly drive their startup innovations to scale (and reaping premium compensation for their role as innovators along the way).

These “business platforms” — the corporate acquirers of technology — still play an essential role in the economy, but it’s not as engines of innovation or magnets for top talent. Instead, the most active tech acquirers — Google, Apple, Amazon, Microsoft, Facebook, Salesforce, VMWare, etc. — make it possible for the best entrepreneurial ideas to achieve global scale, operational excellence and ongoing incremental enhancement. In effect, the role of the multinational corporation is increasingly to maximize the value and financial performance of the innovations they source from the startup community, as opposed to nurturing and developing innovation as a core competency of the organization.

None of the above is strictly true today — every big tech incumbent began life as a startup, and some (most notably Amazon) have been able to hold on to key aspects of their innovative and entrepreneurial startup culture despite having achieved massive scale — but it’s not hard to see evidence for the trend playing out across the economy:

Powered by the overlapping engines of Software-as-a-Service (SaaS), Cloud and Mobile, almost every core enterprise function has been sliced up and farmed out to distributed teams, many of whose members are not full-time employees of the corporation but independent contributors retained — either individually or through a vendor relationship — for their specific skills and expertise.

A huge army of skilled temporary “knowledge workers” — beginning with those who perform mundane tasks, but steadily moving up the skill curve to more elite providers — can now be sourced from global marketplaces like Mechanical Turk, oDesk, Elance, Sortfolio and AssociatedContent. Big companies are already struggling to attract top-tier talent, and services like these provide a welcome alternative to recruiting and retaining full-time employees to perform these roles. Technology advances have compounded these effects, shifting many once-sacrosanct enterprise functions (especially in IT) to cloud-based software platforms owned and operated by someone else and rented by the drink.

As with many global trends, there are troubling social implications to this accelerating disaggregation of the enterprise. If — as it appears — both private enterprise and the state are making a permanent shift away from long-term financial stewardship of the workforce, those who can’t afford to develop and maintain skills relevant to the knowledge economy will have few places to turn for steady employment that earns them a living wage.

These changes will have broad and unexpected ripple effects as well. As just one example, a freelance economy undermines one of the foundations of consumer lending: the paystub. Qualifying a borrower with variable income is difficult, and risk-averse lenders will limit credit and boost borrowing costs to compensate for this uncertainty, further penalizing low earners at the bottom of the skill pyramid. Across the board, the disaggregated economy will become more efficient, but also much harder for the un- or under-trained to participate in.

Uncomfortable as these changes may be, the genies of globalization, technological change and economic fragmentation aren’t going back in the bottle anytime soon. Hang on to your hats, because these trends are only going to accelerate until something breaks…